Executive Summary

- Our living planet, with its biosphere and climate system, has changed at unprecedented speed since the world’s nations gathered in Stockholm in 1972. Changes in the climate and Earth system, which were assumed to unfold in a distant future and only affect future generations, are happening now, with increasing speed and force. We now live in a fundamentally new planetary reality where we are more connected, where the climate system is destabilized, and where the biosphere that supports humanity is becoming more fragile and depleted. This new reality has repercussions for life on Earth, and needs to be the basis for actions aiming to transform the financial sector and our economies towards just futures on a thriving planet.

- Investments are key to a transition to climate stability and biosphere stewardship. Investments impact on key biomes linked to “tipping elements” in the Earth system, and on ecosystems and people who depend on these all over the world. A changing planetary reality creates new systemic risks through domino-effects and feedbacks to economies and the financial sector, which are poorly understood and dealt with today. Financial institutions that mediate these investments play a central part to our ability to shift economies in a direction that promotes a thriving planet for all.

- The responsibility for the new planetary reality lies heavy on high-income countries who represent only 16 % of the world population but whose consumption today is responsible for 74 % of global excess use of natural materials, including biomass, metals, non-metallic minerals and fossil fuels. Moreover, the risks created by our changing planet are not shared equally. Low-income countries with limited historic responsibility are among those suffering the most from the impacts of growing Anthropocene risks. These dynamics further reinforce the already staggering global inequalities.

- The new planetary reality requires us to rethink the indicators for human well-being, macroeconomic performance and financial risks. Indicators for human development must acknowledge human pressures causing the transgression of planetary boundaries and their effects on well-being. Macroeconomic performance indicators need to embed the deep uncertainty engrained in biosphere dynamics to ensure the preservation of natural capital. Financial institutions must recognize a wider set of planetary changes, and develop impact accounting as a core part of capital allocation decisions, and support the open disclosure of Environment, Sustainability and Governance (ESG) data and criteria.

- Economic and financial actors are not equally influential in today’s globalized economies. “Keystone actors” corporations, financial giants, central banks, and index providers must play a larger role in helping accelerate action for sustainability, and especially in parts of the economy of importance for the stability of the climate system and the resilience of the biosphere. Engaging with such influential economic and financial groups offer possibilities, but transparency, accountability and strengthened regulation will be key to secure outcomes that benefit sustainability ambitions and a just transition.

- Large-scale behavioral change has a crucial role to play in a shift towards just futures on a thriving planet. Changes in social norms can instigate such wider changes in society, economies and in the financial sector. Policies can be leveraged to shift norms by altering the behaviors of key actors and by changing expectations. This can result in the activation of large-scale behavioral tipping as actions trigger additional actions. Recent international public opinion surveys, the rise of global youth movements, and current sustainability initiatives by influential actors in the economic and financial sector, indicate that the time might be ripe for such policies that help bridge the gap between sustainability rhetoric and action.

- A changing planetary reality poses immense challenges and risks. Yet, a shift towards a just future for all on a thriving planet is possible, and will require actions from the financial sector, macroeconomic institutions and policy-makers that support transformative capacities. Such capacities entail the ability to define a new direction; create enabling conditions; actively contribute to a phaseout of harmful investments and economic activities in a just way; and to help scale up investments for resilience. Financial and economic incentives can, and should, align with system opportunities and acknowledge the need to sustain critical Earth-system processes in support of the biosphere and human well-being for all.

Preface

“Whether humanity has the collective wisdom to navigate the Anthropocene to sustain a livable biosphere for people and civilizations, as well as for the rest of life with which we share the planet, is the most formidable challenge facing humanity.”

This was the key message and conclusion from the Nobel Prize Summit hosted in 2021. It resembles in many ways the outcomes of the Stockholm conference in 1972, the first ever United Nations conference on the human environment. Fifty years have passed since that historic conference, and while the world is a very different place today, the message remains the same. Astounding progress in human well-being for many and technological breakthroughs have come at the cost of growing social inequality and an increasingly evident climate crisis. Humanity has become a force of planetary change threatening to erode the fabric of life. Yet this daunting prospect of the future is countered by a growing desire to tackle these challenges applying insights from an increasingly vibrant field of sustainability sciences and a formidable human capacity to innovate. Securing a safe and prosperous future for all is still possible.

This report explores the direction the financial sector and our globalized economy need to take to change course. It is a major task, and we present our views with urgency and humility. The insights presented here build on decades of collaborative work within systems thinking, ecological economics, resilience science and Earth system science. It is based on the legacy of the Beijer Institute of Ecological Economics, the Global Economic Dynamics and the Biosphere Program (both at the Royal Swedish Academy of Sciences), and the pathbreaking work done by colleagues associated with the Stockholm Resilience Centre (Stockholm University).

Stockholm+50 offers a unique opportunity for the world to reflect on its progress and failures since 1972. This report offers an important synthesis of how our economies and the financial sector can contribute to this reflection, all with the aim of accelerating towards a more sustainable and just future.

Chapter 1 – A New Planetary Reality

Our living planet, with its biosphere and physical climate system, is changing at unprecedented speed. Changes in the climate system and the biosphere, which were assumed to unfold in a distant future and only affect future generations, are happening now with increasing speed and force. We now live in a fundamentally new planetary reality where we are more connected, more connected, at the same time as more abrupt and sometimes irreversable changes happen, the climate system is destabilized, and the biosphere that supports humanity is becoming more fragile and depleted. This new reality has enormous repercussions for all life on Earth, and needs to be the basis of discussions, strategies and actions about how to transform towards just futures on a thriving planet.

Earth has a biosphere, a thin veil around Earth’s surface where life flourishes. Earth is the only place we know where a complex web of life exists. We humans have emerged and evolved within the biosphere. Our economies, societies and cultures are deeply embedded within it. The biosphere is our home (Folke et al., 2021).

This chapter summarizes key scientific insights about our changing planet, and the implications for prosperity and development for all. It elaborates how and why climate stability and biosphere resilience are key to prosperity and development, and how the scientific understanding of our complex Earth system has evolved over the 50 years since the Stockholm Conference of 1972. The insights emerging from this body of work are far from trivial. Instead, they highlight how the conditions for collective action within and across national boundaries have fundamentally changed during the last decades. They also force us to rethink the organization of our economies, and the role and responsibility of the financial sector in the Anthropocene epoch – the Age of Humans.

Climate change and the Anthropocene biosphere

Human society has developed and flourished during a remarkably stable period in Earth’s history, the Holocene, when global average temperatures varied no more than around 1°C during about 10,000 years (Steffen et al., 2015b). Over the last three million years, the average temperature on Earth has not exceeded 2°C above (inter-glacial) or 4-5°C below (deep ice age) the pre-industrial average temperature on Earth (14°C). Already now at 1.2°C warming above pre-industrial levels (IPCC, 2018), we have moved out of the stable and accommodating Holocene environment of the last 10,000 years with its well-defined and foreseeable seasons that allowed agriculture to develop and complex civilizations to flourish. The projected changes to the climate system in the next fifty years could be larger and more disruptive than humanity has experienced since the beginning of civilization (Steffen et al., 2018). The impacts on societies, vulnerable communities and ecosystems are far from trivial as elaborated by the Intergovernmental Panel on Climate Change (2022).

However, the climate system and the biosphere are more than just the basis for human civilization. As Folke and colleagues (2021) notes, the biosphere and the Earth system have coevolved with human activity over time, creating a close and inseparable inter-dependence between social conditions, health, culture, democracy, power, justice, human security, and the Earth system and its biosphere.

Since the end of the Second World War, the global human population has increased substantially, while on average also becoming much healthier and prosperous. This was enabled by substantial consumption of resources from the planet’s oceans, rivers, forests, grasslands and coastal plains and other landscapes, together with a dramatic rise in telecommunications, tourism, and foreign direct investment, all driven by rapidly growing economies across different regions of the now globalized world (Steffen et al., 2015a). As we elaborate in Chapter 4, the benefits and risks of this acceleration have not been distributed equally.

Figure 1 | A changing planet. Our living planet and the climate system have been transformed fundamentally in the last decades through the ‘Great Acceleration’ – the dramatic growing impact of human activity on the Earth system. Source: (Steffen et al., 2015a).

One of the most prominent frameworks to summarize how the Earth system and the biosphere underpin human prosperity in fundamental ways, is the notion of ‘planetary boundaries’ which identify a “safe operating space for humanity.” (Rockström et al., 2009). This space is defined by a number of dynamic Earth system limits beyond which the stability of the life-supporting conditions on our planet becomes uncertain and might drastically change. Threats to this safe operating space include global warming, loss of biosphere integrity (biodiversity loss and ecosystem resilience), chemical pollution and the release of novel compounds, ocean acidification, freshwater consumption and the global hydrological cycle, land system change, nitrogen and phosphorus flows to the biosphere and oceans, atmospheric aerosol loading and stratospheric ozone depletion. The “planetary boundaries” framework has been refined over the years (such as by Steffen et al. 2015b; Persson et al., 2022; Wang-Erlandsson et al., 2022). It has also been noted that the global framing of such boundaries could be misinterpreted in ways that ignores local and regional realities and changes that take place within such defined “boundaries”, but still undermine adaptive capacity with detrimental impacts on both people and planet (Biermann et al., 2016; Aguiar et al., 2020).

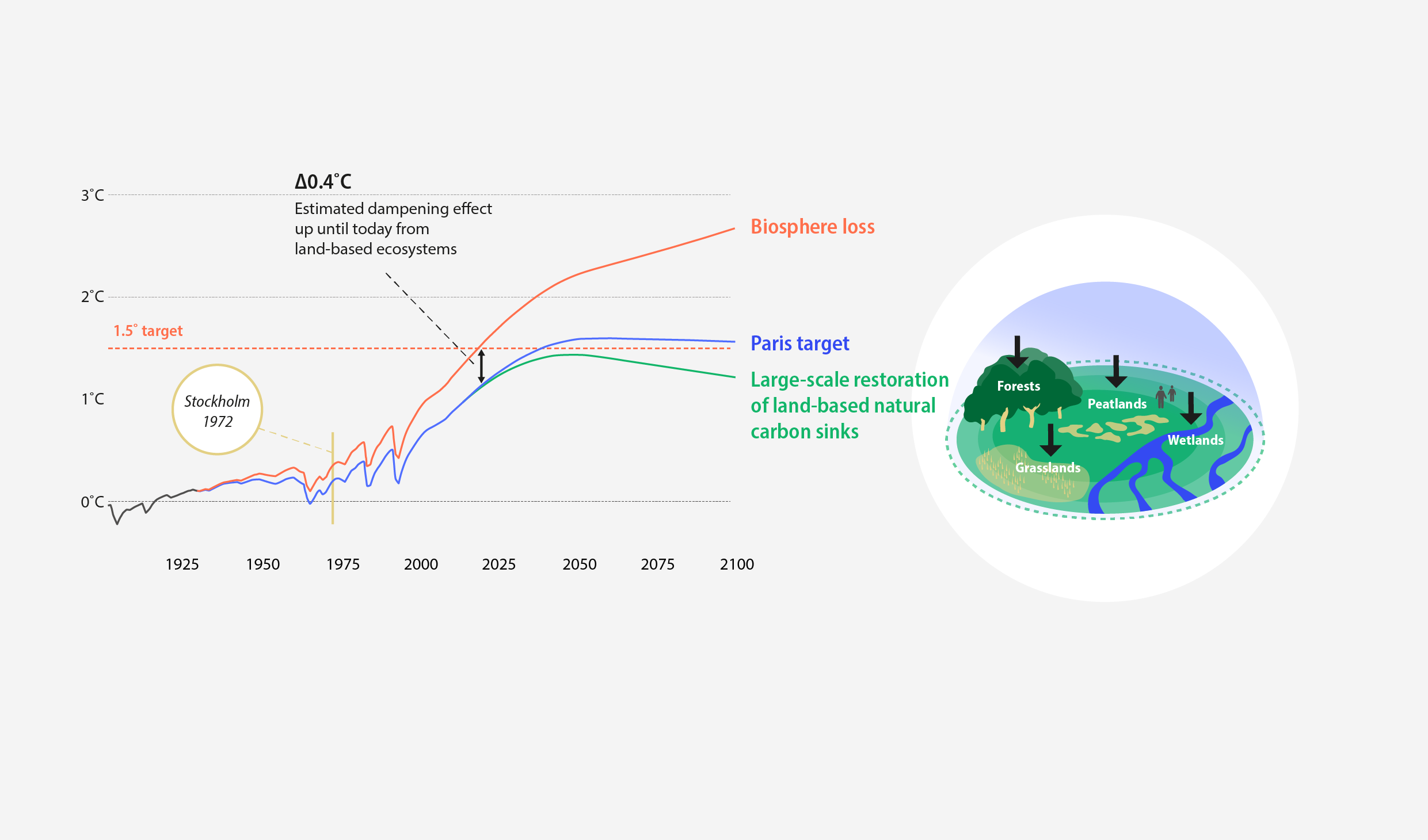

The stability of the climate system is fundamentally dependent on the resilience of our living planet – the world’s oceans, forests, grasslands, wetlands, soils, other ecosystems, and the biodiversity they entail. Biomes such as the Amazon rainforest and the world’s boreal forests store an equivalent of about 10 years of global emissions of greenhouse gases (Steffen et al., 2018). Oceans absorb about 25% of our annual carbon emissions, and over 90% of the additional heat generated from those emissions. Forests, wetlands, and grasslands sequester almost 30% of carbon emissions from human activities. The total amount of carbon stored in terrestrial ecosystems like soil, and living plants is almost 60 times larger than the current annual emissions of global greenhouse gases from human activities (from Folke et al., 2021). Recent analyses show that the world would have already breached the Paris Accord 1.5°C-target already today without the capacity of the living planet – our oceans and land-based ecosystems – to absorb human carbon emissions (Rockström et al., 2021). However, this capacity cannot be taken for granted with continued greenhouse gas emissions, and the loss of resilience of the biosphere (Steffen et al., 2018).

Figure 2 | The importance of the biosphere for the Paris target. The world would already have breached the Paris target without the carbon sinks provided by a resilient biosphere. Source: (Rockström et al., 2021).

{kind=link}

Ecosystems also help reduce vulnerability to climate hazards and extreme events (Diaz et al., 2019), and are key for the achievement of the Sustainable Development Goals (Reyers & Selig, 2020). Mangrove forests for example, safeguard 15 million people against flooding every year, and provide at least US$65 billion in flood protection (Menéndez et al., 2020). Hence it will not only be critical to curb human-induced climate change directly through reduction of greenhouse gas emissions, but also to enhance the regenerative capacity of the biosphere and its diversity, to anticipate and adapt to extreme events, and support and sustain societal development for all within a safe operating space.

Simplifying the planet

These shifts in the climate system unfold in parallel with other unprecedented changes: a mass extinction and the simplification of the biosphere through dramatic transformations of land and seascape, all the way down to the deepest oceans (Nyström et al., 2019; Jouffray et al., 2020). While this transformation has been accompanied with considerable social benefits such as increased and stable food production, it has also resulted in losses of diversity and resilience, which make ecosystems and societies more vulnerable to the repercussions of a changing climate (Hendershot et al., 2020). Resilience refers to the capacity to live and evolve with changing circumstances, predictable or surprising, incremental or abrupt. It includes not only how to persist and adapt to changing circumstances, but more importantly, also the capacity to transform towards sustainable futures by preparing for and making use of the windows of opportunity that change provides (Folke et al. 2021).

Human activities have directly altered at least 70% of land surface, approximately 85% of wetland area and over 66% of the ocean (Diaz et al., 2019). Nearly 40% of all productive land and 70% of global freshwater is being used for agriculture (Foley et al., 2011). Perhaps most shocking, over 96% of Earth’s mammal biomass is now accounted for by people and our livestock – with less than 4% made up by elephants, whales, moose, monkeys and other wild species (Bar-On et al., 2018). Moreover, the increase in agricultural crop production in the last decades has been achieved through an ever-increasing reliance on fewer global crop commodities that are produced and exported from an increasingly limited number of countries (Heslin et al., 2020). 80% of the world’s population today lives in countries that import more calories than they export (Kummu et al., 2020).

These trends are paralleled by an overall homogenization of the food produced globally (Khoury et al., 2014, Nyström et al., 2019; Díaz et al., 2019). Such homogenization results in losses to the pool of genetic variation that underpins the long-term resilience of agricultural and food production in the face of environmental change (IPBES 2019), as well as the increased use of pesticide and herbicide due to the loss of insect diversity and natural pest control (Klein et al., 2007; Potts et al., 2010). According to estimates, loss of animal pollinators – mostly bees – affects more than 75 percent of global food crop types (Klein et al., 2007) and puts $235 billion to $577 billion in global crop output at risk annually (IPBES 2019), with inequitable implications for human nutrition (Chaplin-Kramer et al., 2014).

By transforming much of the planet into cropland monocultures, forest plantations, filled wetlands, and fish farms, humans have changed the properties of the biosphere to such an extent that new types of global risks could emerge that affect the long-term ability to provide food, fibres, fuel, and jeopardize food security for a growing and wealthier human population (Nyström et al., 2019). Shocks previously occurring locally within one sector risk becoming ‘globally contagious’ and more prevalent as sectors are intensified and become more intertwined (Keys et al., 2019). For example, droughts or crop pest outbreaks can spill over to seafood production, since fish farms increasingly depend on agricultural crops to produce their feed. Gains in resource efficiency and production often trade off with the cultural diversity (e.g., through small-scale food production systems) that underpins collective well-being in different ways across the globe (Sterling et al., 2017).

Since the world’s governments gathered at the Stockholm Conference in 1972, not only the continents, but also the ocean has seen an unprecedented increase in the intensity and diversity of uses. From the shoreline to the deep sea, these rapid human-driven changes on the oceans known as the ‘Blue Acceleration’ are having major social and ecological consequences, and raise serious concerns about potentially unsustainable growth trajectories and systemic inequity in the current ocean economy (Jouffray et al., 2020; Österblom et al., 2020). Most benefits accrue to a small portion of the global population, while most harms, including those from climate change impacts, fall on the most vulnerable.

Emerging diseases and the loss of diversity of life

New diseases and agricultural pests are an increasingly disruptive force to society. Commonly referred to as emerging pests and pathogens (EPPs), they include insects, plants, or microbial organisms. Their effects range from impacts on food security, biodiversity conservation, and natural resource management, to those of social equity, health, and safe technology (Jørgensen et al., 2019). Three forces of global change drive the trend of EPPs as a growing sustainability challenge (Carroll et al., 2014; Jørgensen et al., 2019). First, as human land use expands to take up more than 75 % of the Earth’s ice-free land surface, potential EPPs are likely to come in first contact and emerge globally in human habitats. Second, denser human trade and travel networks mean EPPs are more likely to spread between continents and to emerge regionally. Third, human use of technological inputs—such as biocidal agents in resource production and health systems—has increased exponentially and acts as a selective agent for re-emergence through the spread of resistant or more virulent variants. While pandemic pathogens are an obvious example of the large consequences EPPs can have on society (Galaz et al., 2017), they are but a small and unrepresentative sample of the diverse influx of EPPs to society, and their possible domino-effects on society.

One related feature of our new planetary reality is the decline in the habitats available for all animal and aquatic life within the biosphere (e.g., Powers & Jetz 2019; Segan et al., 2016). As just one example, on average, large terrestrial mammals have been extirpated from 75% of their natural ranges since the evolution of modern humans (Faurby & Svenning, 2015). With decreasing forests, poorer freshwater and marine habitats, and declining food availability for non-human species, the number of species currently threatened with extinction is unprecedented in human history: an estimated 1 million species of animals and plants (Ceballos et al., 2015; Ceballos et al., 2017; Díaz et al. 2019). Why does this matter? It matters because species and biodiversity perform critical functions in the biosphere, functions that generate essential ecosystem services to human wellbeing, that provides predictability, stability, and insurance in the flow of such services, and that builds resilience to meet uncertainty, surprise and the unknown.

Another driver behind the new planetary reality is the rapid urbanization of what has been referred to as the “urban century” (Elmqvist et al., 2019). The majority of the world population now live in urban areas, for the first time in human history (UN Population Division, 2018). Urbanization of the world population has come with benefits such as access to education, health facilities and jobs, but also bring negative consequences such as social disparities, insecurity, pollution, loss of biodiversity and lack of contact with nature that all affect urban mental health (Ventriglio et al., 2021). Cities both cause pressures and have to deal with their planetary-wide impacts on the climate and the biosphere. While urban areas are responsible for 70 % of global greenhouse gas emissions, 90 % of cities are situated along coastlines and thus increasingly vulnerable to the effects of global warming (Elmqvist et al., 2019). While actions to address local sustainability challenges on city levels are often needed, it is key to consider global biosphere effects and spill-overs beyond city as well as country borders (Engström et al., 2021).

Connectivity, complex systems and tipping points

The impacts of increased global connectivity and complexity today differ from those identified by the international community in Stockholm in 1972. They are another key feature of our new planetary reality that creates novel challenges and opportunities for policy-making, the finance sector, and society.

The anatomy and impacts of global connectivity for sustainability have gained considerable interest amongst sustainability scientists in the last decade. The mechanisms for these complex cross-sectoral and cross-regional connections are often referred to as ‘telecoupling’ (Liu et al., 2015). This terminology has its roots in the climate sciences, and the phenomena due to what is known as ‘teleconnection’, whereby climate and environmental change in one region of the world can drive weather and environmental changes in another (Diaz et al., 2001). It has become clear, however, that similar cross-continental connections can emerge through economic activities, trade connections, transportation networks, financial economic linkages, and information flows. Examples include policy-induced land use changes in one region that influence precipitation patterns in other countries (Keys et al., 2012), and deforestation policies adopted in one country that lead to additional forest extraction and degradation in others (Meyfroidt et al., 2010). Global changes such as trade patterns, capital flows and information availability increasingly shape local vulnerabilities and opportunities. Such connectivity creates difficult challenges for the problem-solving capacities of institutions and policy-making. Spill-over effects and unexpected consequences of economic and policy decisions are common, and will require novel governance approaches with the ability to steer away from systemic risks, and identify and mobilize action where synergies for both people and planet are possible (Galaz, 2019; Bowen et al., 2017; Engström et al., 2021; Folke et al., 2005). As Brodie Rudolph and colleagues (2020) note however (and as we elaborate in detail in Chapter 7), such connectivity also offers opportunities to support transformations. Networks of innovators can share insights faster in ways that accelerate learning, as well as mobilize collectively to create enabling governance structures.

Key aspects of these global changes are technological advances and their wider impacts on behavior, norms, economies and institutions (Arthur, 2011). The acceleration and expansion of human activities into a converging globalized society have been supported by the discovery and use of fossil energy and by innovations in social organization, technology, and cultural evolution (Ellis 2015; van der Leeuw 2020). Further technological innovation and change such as advances in robotics, synthetic biology and artificial intelligence are likely to continue shaping Earth’s life support system and offer both opportunities and risks (Folke et al., 2021; Galaz et al., 2021).

The sum of all of the technological objects manufactured by humans, or the so-called “technosphere”, is a fundamental part of our changing planet. It’s weight on the planetary system is estimated to be on the scale of 30 trillion tons, or 50 kilos for every square meter of Earth’s surface (Zalasiewicz et al., 2017). Technological innovations are giving this infrastructure the ability to process information continuously, reason, remember, learn, solve problems, and at times even make decisions with minimal human intervention through artificially intelligent machines and increased automation (Markolf et al., 2021). Hence, we face not only unprecedented climatic and ecological conditions, but also the influence of increasingly intelligent autonomous systems with the ability to create novel connections between the social, the ecological, and the technological (Galaz et al., 2021).

But the world is not only increasingly connected and changing at an unprecedented speed. Some of these connections evolve into what can be defined as complex adaptive systems (Levin, 1998; Folke, 2006). Such systems are prone to abrupt, and at times irreversible, shifts with important implications for human development. The terminology differs between different fields of research, including regime shifts, catastrophic shifts, tipping elements, and tipping points, describing a system that crosses a critical threshold and shifts to a significantly new system trajectory or pathway (Lenton, 2013; Rocha et al., 2018; Scheffer et al., 2001). Evidence of such shifts can be found in multiple social-ecological systems and at multiple geographical scales from the local (e.g., a lake) to the global (e.g., the Earth system). Many shifts are associated with the loss of key ecosystem services that underpin livelihoods, economic activities and human development (Biggs et al., 2018; Lenton et al., 2008; Rocha et al., 2018).

‘Tipping elements’ in the climate system are a good illustration of these phenomena. The melting of sea ice on the Greenland and Antarctic ice sheets is one example as the melting surface changes its reflective properties resulting in self-reinforced warming. The alteration of critical biomes such as the large forests in the Amazon basin and the boreal forests in Canada and the Russian Federation is another example of interacting changes that could lead to the transgression of tipping elements (Lenton et al., 2008; IPCC, 2021).

Many of these biomes identified as critical for the climate system are changing rapidly because of a combination of direct and indirect human pressures. The potential tipping of the Amazon rainforest into a savanna or open woodland is being driven by the combined stresses of climate change and direct human-driven deforestation due to expanding soy plantations, for example (Nobre et al., 2009; Galaz et al., 2018b). The human activities that drive the Great Acceleration are rapidly changing the internal dynamics of many tipping elements (Lenton et al., 2008; Lenton et al., 2019), subsequently risking the long-term stability of the climate system through proposed tipping cascades (Steffen et al., 2018).

The precise timing and impacts of such abrupt shifts on people and their well-being are highly uncertain (Hoegh-Guldberg et al., 2018; Wang & Hausfather 2020; IPCC, 2021). Another complicating factor is the fact that such abrupt shifts can result in domino effects between climate and ecosystems with potentially large, yet unquantifiable impacts on economies and livelihoods. A recent synthesis based on 300 case studies and a review of more than 1,000 academic papers (Rocha et al., 2018) shows that ‘regime shifts’ in one biome or ecosystem can trigger similar irreversible shifts in other biomes, sectors and/or regions. One clear example is the atmospheric recycling of moisture, whereby moisture captured in vegetation evaporates, and is transported in the atmosphere over long distances before falling down in another location as precipitations. The Amazon rainforest for example, depends on moisture recycling as an important water source, and large disturbances in this cycle could lead to shift of this biome from rainforest to savanna. Changes in moisture recycling in the Amazon can also affect mountain forests in the Andes as well as nutrient cycling in the ocean by altering sea surface temperature, which leads in turn to regime shifts in marine food webs. As Gleeson and colleagues (2020) explore, such complex connections between the biosphere and hydrological cycles should be investigated at the planetary level.

At times however, such abrupt shifts can also unfold in social systems in ways that result in positive shifts towards sustainable pathways (Otto et al., 2020). We elaborate examples such as these in Chapter 6.

Understanding Anthropocene risks

Complex systems and increased connectivity through ‘telecouplings’ can both enhance and undermine the resilience of people and planet. Remittances can help families cope with a suite of problems in troubling times (Adger et al., 2002; Naudé & Bezuidenhout 2014). Global information and communication technologies have proven critical to help coordinate national responses and facilitate information sharing between scientists during the COVID-19 pandemic. Local and national vulnerability to food scarcity and shocks has been mitigated partly through international food trade (Porkka et al., 2013). However, global connectivity can also result in independent cascading failures such as ruptures, shocks or propagating disturbances, known as globally networked risks or systemic risks (Helbing 2013; Centeno et al., 2015).

There is a growing interest in the environmental and ecological dimensions of such risks, including climate change, deforestation, extreme weather events and natural resource constraints (UNDP, 2020; Galaz et al., 2017; Keys et al., 2019). As the recent increases in food prices all over the world illustrate, while international food trade can help mitigate local stresses food production, it also creates transboundary connections that allow for shocks to food production to cascade through the global network of agricultural trade (Heslin et al., 2020). Furthermore, resource extraction facilitated through trade has created vast geographical connections where environmental degradation in one country is hidden or masked through complex supply chains. Transboundary food trade for example often masks unsustainable groundwater extraction in food producing countries (Dalin et al. 2017). Global seafood trade allows countries and corporations to compensate for species loss from local marine ecosystems (Crona et al., 2016).

The speed, scale and connectivity of the Anthropocene lay the foundation for challenging and unevenly distributed ‘Anthropocene risks’ (Galaz 2014; Keys et al., 2019). Stresses and shocks can move swiftly from local to global and back again. They may also interplay across sectors in a society, rapidly affecting ecosystems, food security, economies and human health. Such risks and their impacts on human development are however difficult to quantify with greater precision due to their multilevel and complex adaptive system properties (Keys et al., 2019). The impacts of a changing planet on human development will not only depend on changes in frequencies and magnitudes of shocks, such as droughts, floods and extreme weather events, but also on the anatomy of connectivity across land, oceans and climate, as well as the vulnerability of important biomes and ecosystems underpinning human development.

These examples illustrate an important shift in the state of our planet, and in our capacities to deal with such disturbances. The fact that our planet has been transformed from forested landscapes, living oceans, and biodiverse ecosystems to simplified and increasingly homogenized production systems, increases social and ecological vulnerabilities to long-term change and abrupt shocks. These may lead to abrupt biosphere changes, changes that a previously resilient biosphere could absorb.

The networked features of global change and the resulting risks that emerge from them create a new planetary reality. Our economies and the financial sector play a key role as societies strive to avoid maladaptation and instead enhance resilience including transformative capacities (Olsson et al., 2022; Biggs et al., 2012, Folke et al., 2005) to what is likely to become a more turbulent future.

Chapter 2 – Finance and Our Living Planet

Investments are key to a transition to a net-zero world, climate stability and biosphere stewardship. The institutions that mediate these capital flows are therefore central to our ability to shift our economies in a direction that promotes a thriving planet. This chapter elaborates how investments impact on key biomes linked to “tipping elements” in the Earth system, and ecosystems all over the world. It also presents a synthesis of current understanding of domino-effect and feedback risks between climate, ecosystems and the financial sector. The chapter concludes with a discussion about how a new planetary reality changes the way systemic risks are understood and dealt with in the financial sector.

Investments, and the financial institutions mediating capital flows, are increasingly viewed as instrumental for the transformation needed to achieve a prosperous future for all (Crona et al., 2021). Today’s globalized economy relies heavily on the financial sector to allocate capital for its operation. The influence and responsibility of financial actors to contribute to a transformation towards a just and safe future for all thus becomes increasingly clear, particularly for economic sectors that have tangible impacts on ecosystems and people’s livelihood dependencies. Examples include tropical and boreal forests (Galaz et al., 2018a), oceans (Jouffray et al., 2020), and many habitats around the world which are critical for biodiversity, indigenous communities and for sustaining ecosystem services (Yang et al., 2021; Dempsey et al., 2022).

The growing interest in “green,” “net zero,” or “climate friendly” investments in the last decades is in many ways a reason for hope. The number of signatories of the Principles for Responsible Investment (PRI) reached 4,000 this year (Segal, 2021). A synthesis conducted by the Global Landscape of Climate Finance (2021) recently showed that total climate-related financial investment has steadily increased over the last decade, reaching USD 632 billion in 2019/2020. New estimates show that almost 40% of all assets managed in European Union-domiciled funds in 2021, are marketed as “sustainable” (Wilkes, 2022). The International Monetary Fund’s analysis show a similar global trend with a record-high growth in 2021 for Environmental, Social and Governance (ESG) debt issuance reaching USD $1.6 trillion (+116% compared to 2020, from IMF, 2022). This growth is likely to continue as countries and financial institutions such as the Glasgow Financial Alliance for Net Zero (GFANZ) and multilateral development banks follow up on their commitments after COP26 and the Glasgow Climate Pact (Robins and Muller, 2021).

The limits of “green” and “sustainable” investments

While this growing interest should be a cause for optimism, there are still considerable challenges facing the world’s ambitions promote transformations towards sustainable societies and economies through an increased engagement from the financial sector. For example, while ESG and climate investments have certainly seen a rapid growth in the last decade, the increase in climate finance is not yet enough to help achieve the Paris Agreement target of limiting global warming to 1.5°C above pre-industrial levels (Climate Policy Initiative, 2021), nor the ambitions of the Sustainable Development Goals (OECD, 2021). Despite this emphasis on greener investment and the global rhetoric to “build back better” since the beginning of the COVID-19 pandemic, G20 countries have still directed around USD 300 billion in new funds towards fossil fuel activities (SEI et al., 2021).

Recent analyses also show that the combined economic effects of the COVID-19 pandemic in combination with the war in Ukraine are widening the economic gap between rich and poor countries of the world. Many developing countries were forced to cut budgets for education, infrastructure and other capital spending during the pandemic. The war in Ukraine seems to put these countries in an even more challenging situation with higher energy, food and other commodity prices, higher inflation, and increased volatility in financial markets (United Nations Inter-agency Task Force on Financing for Development, Financing for Sustainable Development Report, 2022).

The challenge is not only related to the total volumes of funding, but also to which sectors these investments are directed. The financial sector has for a long time centered their work on sustainability on the reporting of GHG emissions and capture. As a result, financial risks are consistently viewed to evolve from climate change alone, rather than from the wider suite of changes in ecosystems and the Earth system (Crona et al., 2021). While a number of recent initiatives have tried to broaden the scope to also include a wider range of ecological and environmental changes (such as the Taskforce on Nature-related Financial Disclosures: TNFD), it is clear that both governments and investors are underdelivering in preparing for a more turbulent future. For example, of the $3.38 trillion of proposed longer-term post-covid recovery investments, only 15% is currently “green” with a focus on cutting greenhouse gas emissions or air pollution, with just 3% directed towards contributing to a more resilient biosphere (Rockström et al., 2021, p. 4).

The strong interest amongst policy-makers and the financial sector around SDG-classified investments and ESG-funds also overlooks some of the more complex political and economic drivers that undermine the protection and stewardship of ecosystems and the biosphere. These includes (as we elaborate in Chapter 3) harmful subsidies, tax avoidance and evasion, and national debt in developing countries which all pose serious obstacles to the protection of nature and biosphere stewardship (Dempsey et al., 2022; Galaz et al., 2018b). As we also elaborate in Chapter 4, current metrics of Environmental, Social, and Governance (ESG) risk and financial materiality have serious shortcomings, and are not likely to help either governments or the financial sector to prepare to our new planetary reality (Chapter 1).

Finance on a changing planet

This section takes a closer look at how the financial sector is currently contributing to the profound transformation of ecosystems, biomes and our living planet. We also explore the state of knowledge about the combined impacts on the financial sector created by interacting changes between climate and ecosystems.

Sleeping Giants in the Climate System

Large-scale shifts in the climate have occurred in the history of planet Earth before. Climate tipping elements are key to understanding this phenomenon, and for evaluating the risks of such shifts happening again (Lenton et al., 2008). As we elaborated in the previous chapter, both past evidence, climate models and current observations indicate that parts of the Earth System and associated processes can cross shift rapidly, changing their internal dynamics and driving feedbacks with large impacts on the climate system as whole. This is why these tipping elements also have been referred to as “sleeping giants”.

Two important terrestrial ‘sleeping giants’ are the Amazonian and boreal forests. Both are sensitive to rising temperatures and changes in rainfall. These biomes are also under pressure from economic activities, such as logging, mining and deforestation caused by expanding agriculture production. The Amazon rainforest is also the world’s most biodiverse biome and pulls large amounts of carbon out of the atmosphere. It supports the livelihood of millions including indigenous communities (Garnett et al., 2018) and holds between 135 and 180 billion tons of carbon in its soils, trunks and roots (Steffen et al., 2018). Almost 20% of the Amazon forest has disappeared since the 1960’s to give place to infrastructural development and agricultural activity, such as soy production and cattle ranching.

Modeled estimates indicate that the Amazon rainforest is close to crossing a tipping point where major parts of the forest could begin a process of die-off and gradually turn into a savanna-like state. Models estimating such shift, based on only temperature rise or deforestation in isolation, show these to occur at temperature increase of 3-5°C or 40% loss of original tree cover (Salazar et al., 2007; Sampaio, et al., 2007). However, more recent analyses suggest that deforestation in combination with warmer temperatures and increasing forest fires could lead to the transgression of a tipping point as early as at 20-25% deforestation of pristine levels – only slightly more than the current levels (Lovejoy & Nobre, 2018). If the Amazon were to “tip” into a savanna-like landscape it would store vastly less carbon, it would likely burn more often, and taken together it would turn from a net carbon sink to a net carbon source (total carbon flux minus fire emissions). There are indications that this process has already begun (Gatti et al., 2021), and thus all measures to halt this biome’s progress towards a tipping point are necessary and urgent. In its 2021 synthesis, the Intergovernmental Panel on Climate Change (IPCC) noted that abrupt responses and tipping points cannot be ruled out (IPCC, 2021a). IPCC also noted that the Amazon could cross a tipping point during the 21st century due to the combined stresses created by deforestation and a warming climate.

Boreal forests are the largest biome on land and play a critical role in the climate system. These forests sprawl across Canada, Russia, Alaska, and Scandinavia. They comprise about 30% of total forest area on the planet and store vast amounts of carbon (about 340 billion tons). The combination of rising temperatures, as well as increased insect attacks, intensity and frequency of wildfires, and logging activities are leading to decreases in boreal forest cover and increasing carbon emissions. Research indicates that as much as 40 billion tons of carbon could be emitted by boreal forests to the atmosphere by 2100 with a 2°C temperature rise, and even more if a tipping point is crossed. This tipping point is currently estimated to lie somewhere around a 3-5°C rise in global average temperature. Changes in these forests will most likely also affect surface albedo (e.g. dark forests absorb heat, white snow reflects heat), potentially amplifying Arctic warming (from Steffen et al., 2018).

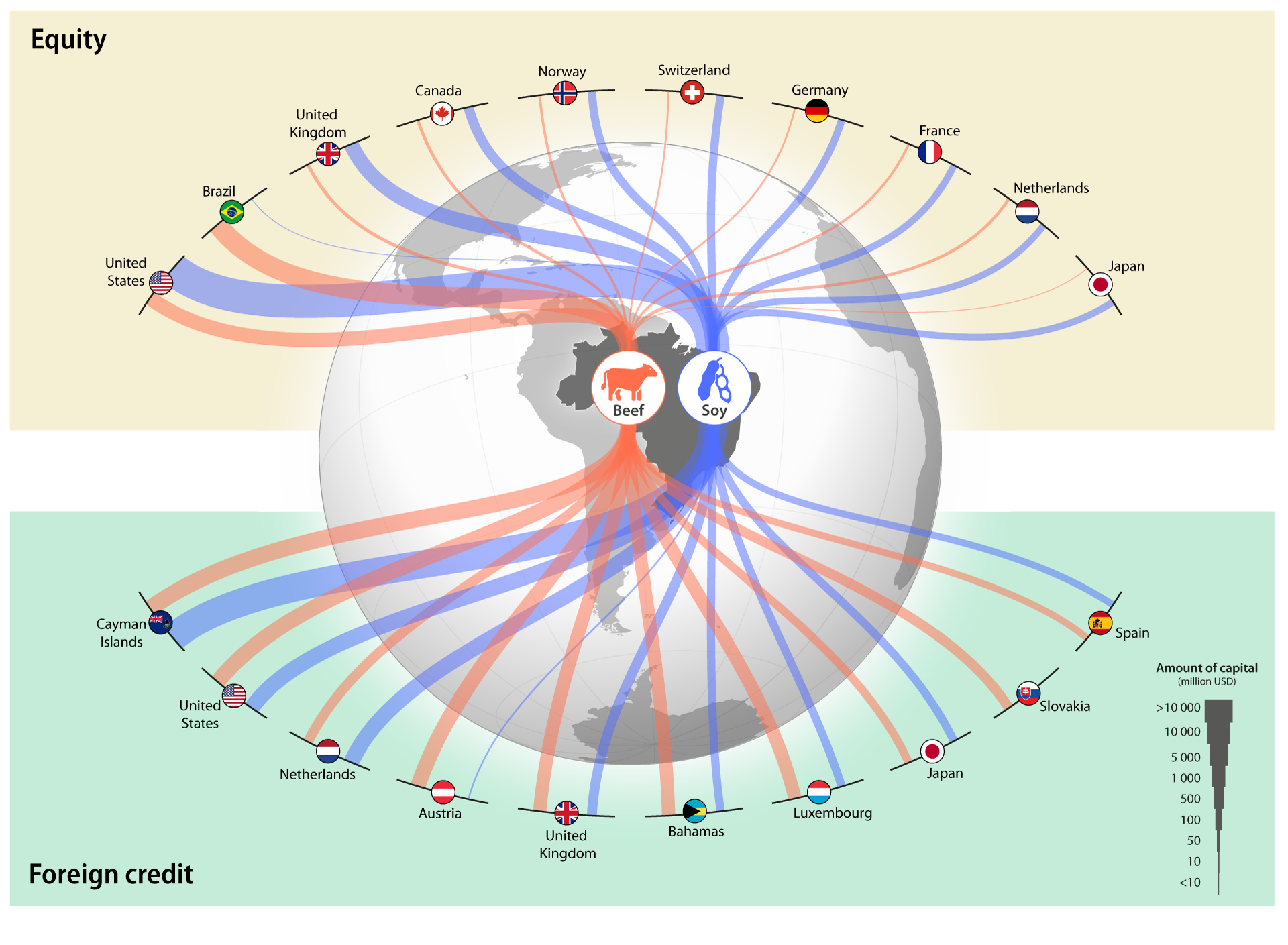

The connection between the financial sector and a changing Earth system might seem vague at first glance. As recent studies indicate, however, financial institutions and investments are contributing to the destabilization of sleeping giants in the climate system (Galaz et al., 2018a, b). In simple terms, investors provide capital through equity, loans and bonds to companies producing or trading soy, beef, timber, pulp, paper, and other commodities. These economic activities constitute stromg drivers behind changes in forests that undermine the stability of sleeping giants, such as the Amazon rainforest and the boral forests. Companies operating in deforestation prone sectors in the Amazon for example, receive considerable financial flows from not only national development banks and other direct subsidies (Nepstad et al., 2014), but also through international loans and payments. Data shows that a majority of the latter capital flows are transferred from or via tax haven jurisdictions, creating serious challenges for transparency and tax fairness, and as a result also for sustainability and biosphere stewardship (Galaz et al., 2018b, we elaborate on this issue in Chapter 3). The direct funding of economic activities that undermine natural capital and resilience is a general and global problem. According to the influential Dasgupta Review on the Economics of Biodiversity, “existing private financial flows that are adversely affecting the biosphere outstrip those that are enhancing natural assets, and there is a need to identify and reduce financial flows that directly harm and deplete natural assets” (p.474) (Dasgupta, 2021).

Figure 3 below illustrates this important point, and shows the two types of investments (equity and credit) to trading companies operating in two major deforestation-risk industries operating in the Brazilian Amazon: soy and cattle. The top of the image shows the investments of the top-10 countries through stock ownership in nine strategically selected companies operating in these two sectors. The bottom of image shows the total credit received by the same companies from corporations and financial institutions (such as banks) located outside of Brazil during the years 2000-2018. The global nature of ownership is notable, with US-based financial institutions clearly on a leading position. Another insight is related to the prominent role tax haven jurisdictions (such as the Cayman Islands and The Bahamas) play for foreign credit to these industries. The selected companies received a total of USD 21.5 billion in foreign credit from tax havens over the period, which represents 57.6% of all their declared foreign credit. As we elaborate in Chapter 3, such extensive uses of tax haven jurisdictions are associated with numerous problems that undermine sustainability and biosphere stewardship.

Figure 3 | Equity, and foreign credit to deforestation-risk economic industries in the Brazilian Amazon. The data from this image is based on the methods and analysis presented in (Galaz et al., 2018a and Galaz et al., 2018b). Updated data from these cases have been provided by Ami Golland (equity, based on data from Orbis values for year 2018) and by Alice Dauriach (foreign credit, based on data from the Brazilian Central Bank, 2000-2018).

{kind=link}

As we elaborate in detail in Chapter 5, many prominent asset managers and financial institutions (including banks and pension funds) also have significant ownership in all sectors connected to the stability of the Amazon rainforest, and also boreal forests (Galaz et al., 2018a). While asset managers are rarely the underlying owners, they can be argued to have a duty of care to their investment beneficiaries to invest and use their influence in ways that promote economically, ecologically and socially sustainable activities. Large asset managers such as the “Big Three” asset managers BlackRock, Vanguard and State Street seem to play an underestimated, yet important role in this context through their relatively large combined ownership in industries with impacts on sleeping giants (see Chapter 5).

This section builds on Galaz et al., 2018b, and Gaffney, et al., (2018). Sleeping financial giants – Opportunities in financial leadership for climate stability. Global Economic Dynamics and the Biosphere programme (Royal Swedish Academy of Sciences), Future Earth, and the Stockholm Resilience Centre (Stockholm University).

Ocean Finance

Our planet’s vast oceans are changing rapidly. The ocean covers more than 70 percent of Earth’s surface, and plays a crucial role in the climate system. It provides ecosystem goods and services that sustain life and support the well-being of billions of people worldwide (Sumaila et al., 2020). The extent of human pressures on the world’s oceans is unprecedented (Jouffray et al., 2021) and result from a changing climate, overextraction, direct habitat damage, and pollution (Sumaila et al., 2020). In parallel, ocean-based industries are growing at an unprecedented pace through technological innovation and increasing human demand for food, energy, material and space. The ocean is widely seen as the next economic frontier and as the solution for sustainable future human development. There are serious concerns, however, regarding who these developments benefit, stewardship of the ocean commons, and the emergence of unprecedented ocean risks that could have large impacts on vulnerable states and communities (Jouffray et al., 2021; Tokunaga et al., 2021; Blasiak et al., 2020).

Ocean finance can play a key role in assisting transformation towards sustainability, both as enablers and gatekeepers. In its first role, the finance sector can help bridge a vast “ocean finance gap” by acting in ways to unlock capital and increase finance to a resilient ocean economy for all. As Sumaila and colleagues (2020) show however, less than 1 percent (USD13 billion) of the total monetary value of the ocean has been invested in sustainable projects with a vast majority supporting large-scale activities that counter the delivery of the Sustainable Development Goals. In addition, SDG 14 (“Life Below Water) remains the least funded goals of all. While an estimated USD175 billion per year is needed to fund SDG 14 (Johansen & Vestvik 2020), it received just below USD10 billion in total over the period 2015-2019 (OECD, 2021).

The financial sector can in principle, act as gatekeepers by deciding what to finance and under which conditions. Indeed, as much as the ocean finance gap is a reality when it comes to sustainable investments, the ‘Blue Acceleration’ also illustrates that billions of dollars are currently entering the ocean economy and fueling the development trajectory of ocean sectors with little if any sustainability consideration. A focus on who and what is financing this Blue Acceleration can therefore unlock powerful leverage points to redirect corporate finance (Jouffray et al., 2019).

Harmful subsidies through for example government payments that incentivize overcapacity and lead to overfishing, for example, remains a major concern. Such subsides not only have major environmental implications, but also threaten low-income countries that rely on fish for food sovereignty (Sumaila et al., 2021). The extensive use of tax haven jurisdictions and the limited engagement by the financial sector on issues of tax fairness also remain as serious obstacles as the world strives to combat illegal and unregulated fisheries around the world (Belhabib & Le Billon, 2020; Ford & Wilcox, 2019; Galaz et al., 2018b).

This section is based on Jouffray J-B, Blasiak R, Nyström M, Österblom H, Tokunaga K, Wabnitz CCC, Norström AV (2021). Blue Acceleration: an ocean of risks and opportunities. Ocean Risk and Resilience Action Alliance (ORRAA) Report.

Zoonotic Disease Risks

Zoonotic diseases are on top of global agendas due to the COVID-19 pandemic. The impacts of emerging and re-emerging infectious diseases on human health and societies can be devastating as illustrated by Ebola, SARS, MERS, and COVID-19 whose impacts propagate through trade connections, travel networks, and fragile health systems and communities (Di Marco et al., 2020). The specific mechanisms that connect factors such as climate change, deforestation and urbanization with the emergence and re-emergence of such diseases are complex (Alimi et al., 2021; Carlson et al., 2021). There is an increasing recognition that various forms of environmental and ecological changes, including deforestation, the expansion of agricultural land, and increased hunting and trading of wildlife can be linked to the emergence of such diseases (Allen et al., 2017; UNEP and ILRI 2020; Di Marco et al., 2020). Zoonotic risks are also likely to increase substantially in the near future due to the combined effects of climate and land-use change (Carlson et al., 2022).

To what extent financial investments affect zoonotic disease risks has yet to be explored in detail however. This is critical because financial investments in economic sectors that increase deforestation risks or that lead to the expansion of agriculture, in addition to their direct impacts, may lead to increased zoonotic spill-over. Indeed, reduced biodiversity, land fragmentation and habitat loss create new patterns of interactions between pathogens, non-human animals, and humans.

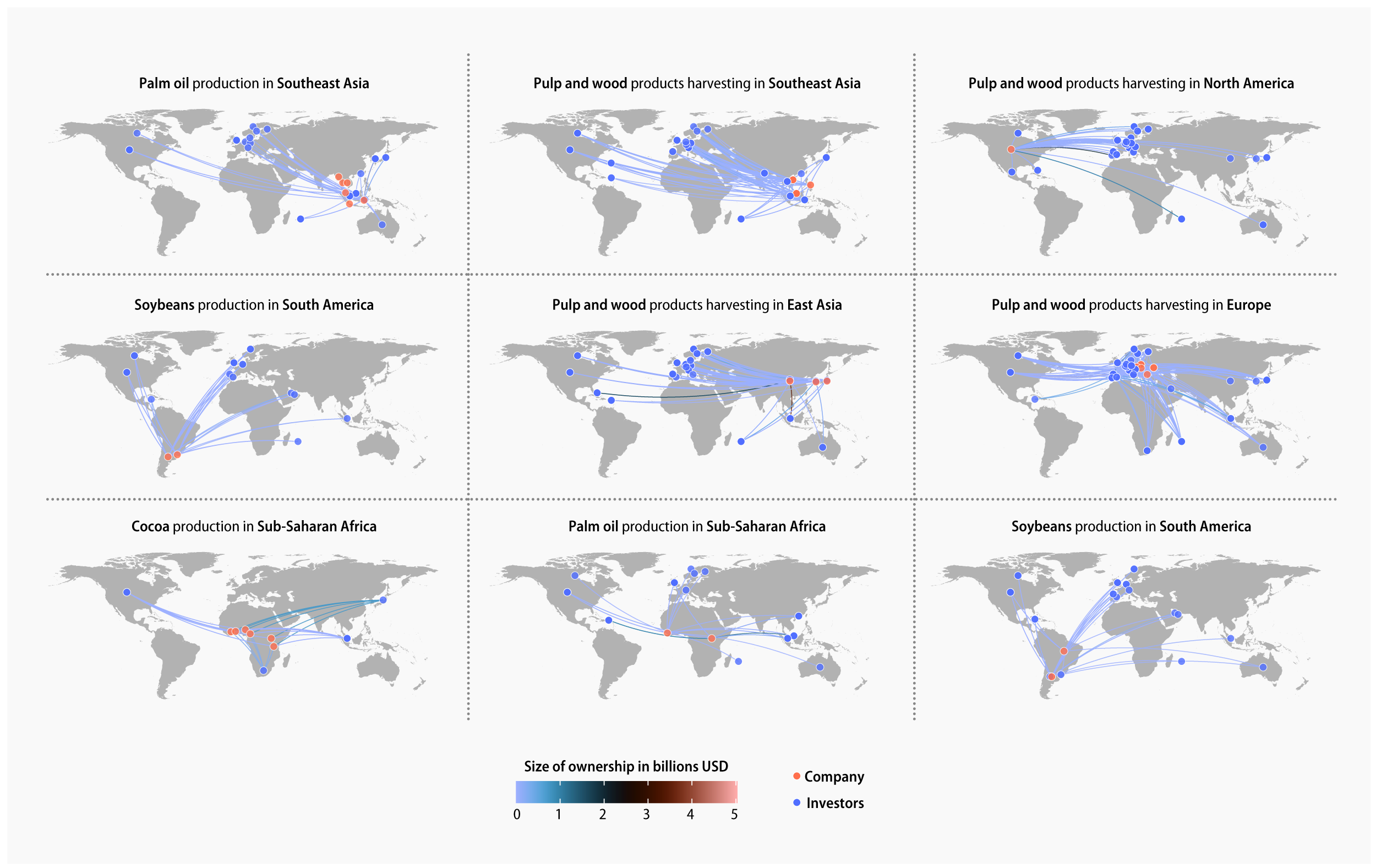

Figure 4 summarizes our analysis of the connection between investments (through equity) in industries with known connections to zoonotic disease risks. The selected circled regions and biomes have been identified by Allen and colleagues (2017) as “hot-spots” where emerging and re-emerging disease risks are primarily driven by anthropogenic land-use change. Our analysis has a number of limitations that we elaborate in (Galaz et al., 2022). It is important to note however, the global nature of financial investments associated with increased emerging and re-emerging disease risks. Quantifying these risks is challenging, but also illustrates the following. First, it illustrates how our changing planetary reality produces novel and poorly understood domino-effects and systemic risks to the finance sector. Second, it shows the responsibility of financial institutions to acknowledge that they are not only influenced by planetary change, but in fact are contributing to these changes directly and with possible large repercussions.

Figure 4 | Global connection of investments through equity. Financial investments shape our living planet, and indirectly also zoonotic disease risks through investments in industries associated with various forms of land-use change in known zoonotic disease hot-spots. The figure shows the global characteristics of such investments in nine identified hotspots, as well as the respective investment size through equity in USD. Purple nodes are where companies and investors overlap geographically. Note that the figure is a simplified data-based illustration. Source: (Galaz et al., 2022).

{kind=link}

Domino-effects and systemic risks

Our understanding of the direct impacts on the financial sector by climate change has grown considerably the last years. However, the largest and least predictable risks of a changing planetary system are likely to be those that emerge from second-order or domino effects, which make them difficult to quantify with precision. Battiston and colleagues (2017) for example, note in their analysis of data for shareholders of listed firms in the European Union and in the United States that climate related financial risks are not only direct, but could be considerable due to the interconnected features of financial investments. The United States Financial Stability Oversight Council noted in its report in 2021, that while climate change could be viewed as an emerging threat to financial stability in the U.S., there was also a critical need to “improve the availability of data and measurement tools, enhance assessments of climate-related financial risks and vulnerabilities, and incorporate climate-related risks into risk management practices and supervisory expectations for regulated entities […]” (FSOC, 2021, p.3).

There is also a growing interest in financial risks resulting from the loss of nature and biodiversity tied to forest, food, and land sector, each entailing complex domino effects between financial investments, climate and ecosystems (Kedward et al., 2020; Crona et al., 2021; see van Toor et al., 2020 for an analysis of these for the Netherlands; McCarthy & Piotrowski, 2022 for the United States; Svartzman et al., 2021b for France; ECB, 2021; Johnson et al., 2021). Biodiversity loss such as the decline in pollinator species for example, could affect global food production and as a result, cause commodity price inflation. Economies that to a larger extent depend directly on the productivity of natural resources such as agriculture, fisheries, forestry, could also see their sovereign debt affected by the loss of biodiversity and the degradation of ecosystem services (Agarwala et al., 2022). For example, recent modeling results indicate that abrupt negative changes in ecosystems by 2030 could be more damaging than the COVID-19 pandemic to Indonesia’s debt sustainability (NFGS-INSPIRE, 2022: p. 50f).

Current risk frameworks also seem unable to grapple with the interactions between climate, ecosystem and financial systems, and the potential for cascades and threshold effects (tipping points) (Crona et al., 2021; NFGS-INSPIRE, 2022). Such complex systems behavior challenges conventional notions of climate risks created by, and to the financial sector. As summarized in (Crona et al., 2021), there is an urgent need to rethink such risks from direct, short-term and linear, to indirect, long-term and non-linear. Our review of the literature in this domain shows that such risks indeed are poorly understood, and thus remain a critical area of inquiry and policy-making (Box 1).

Box 1. How much do we know about financial risks created by domino-effects across climate and ecosystems?

There is a growing recognition that changes in the climate system and ecosystems are closely integrated, posing novel and unfolding risks to the financial sector. Environmental-related risks are often classified into physical and transition risks. Physical risks arise from changes in weather patterns or other environmental changes, such as the impacts of droughts or floods on company operations or physical infrastructure. Transition risks emerge as the result of policies or shifts in consumer values that emerge as a response to, for example, national or international climate targets. Both physical and transition risks are expected to have an impact on the likelihood and magnitude of other financial-related risks including market and credit, insurance, operational, and liability risks. Understanding how interacting climate and ecosystems risks affect the financial sector is becoming increasingly urgent. Our systematic literature review of 75 selected publications shows that, while there is a growing interest in climate related risks, their connections to ecological change is systematically underdeveloped. Existing research including data availability and methods development also have a heavy emphasis on financial risks towards European and USA-based financial institutions, thus ignoring potentially large impacts on fragile countries and other large economies such as India, China and Brazil.

From: Sanchez et al., (2022)

Leverage points for influence

Debt and equity offer potentially powerful pathways for influence in industries that are modifying our living planet and climate system (see Box 2).

Box 2. Understanding the influence of shareholders

Shareholders have three different ways to influence publicly listed corporations: First, investors might (threaten to) divest from companies by selling their shares. Investors in index funds, however, are not able to divest from individual firms because they track entire indices. Moreover, the material effects of divestment have been found to be small at best (Plantinga & Scholtens, 2021; Broccardo et al., 2020; Cojoianu et al., 2021) – even though there may be an important ideational impact by the divestment movement through challenging the ‘social license to operate’ of fossil fuel firms (Jahnke, 2019). The main reason that divestment does not have a significant material effect is that the vast majority of publicly listed firms do not finance themselves by issuing new shares, but via retained profits or by issuing bonds. Hence, it is not possible to ‘starve’ fossil fuel firms of capital by investing only in “green” or ESG funds. Second, shareholders (that is, primarily their asset managers) can use the influence provided by their shares for voting at annual general meetings, including the election of new board members (Krahnen et al., 2021). Finally, asset managers are thanks to their ownership able to influence the top management of their portfolio firms via private engagements. Voting and engagements have been found to offer the highest impact (Kölbel et al., 2020).

Financial influence can at times be concentrated in the hands of a limited number of investors (see also discussion in Chapter 5). Previous research has referred to these powerful investors as “sleeping financial giants” in the case of forest biomes related to tipping elements in the climate system (Galaz et al., 2018b; Gaffney et al., 2018). In partnership with other financial institutions, these investors could help change the destructive path of key biomes. In addition, such giants could help develop investments that explicitly promote the resilience of critical biomes by engaging with companies and forming alliances with similar minded investors. Examples of topics for engagement include measures to achieve effective zero deforestation in supply chains; design of effective and fair tax policies; and the promotion of forest rehabilitation through reforestation, afforestation, and forest management practices protecting human rights and biodiversity (from Gaffney et al., 2018, see also Nobre & Nobre, 2020 for the Amazon, and Astrup et al., 2018 for boreal forests).

There are other ways that the financial sector can – and should – engage to contribute to actions towards biosphere stewardship. Banks for example, are particularly influential given their ability to monitor companies in detail and to tailor loan terms (Jouffray et al., 2019). The so-called Poseidon Principles* for example, provide a sector-specific framework for integrating climate considerations into lending decisions and promoting shipping decarbonization. The signatories – 27 leading banks jointly representing US $185 billion, or about half of global shipping finance – incentivize shipowners to decarbonize their fleets by lowering their interest rate as they decrease their emissions.

Multi-lateral development banks (MDBs) can play an important role as well. MDBs and public sector financing can help de-risk investments by the private sector, and also are a ready source of (too rare) investable projects for private sector investors. Ten multi-lateral development banks recently pledged to “further mainstream nature into our policies, analysis, assessments, advice, investments, and operations, in line with our respective mandates and operating models”.** Together these banks disburse over US $220 billion annually. Over the past decade, they have begun driving this shift, through a suite of nature-positive investment priorities, demonstrated in numerous countries and sectors, and now being scaled and standardized (Mandle et al., 2019).

Stock exchanges are also interesting in the context of sustainability disclosure and performance as they can act as regulatory bodies via their listing rules, both at the time of the listing and on an annual basis. The Tokyo Stock Exchange alone, for example, alone concentrates 53% of the combined revenue of the world’s largest 45 publicly-listed seafood companies, while the exchanges of Tokyo, Oslo, Korea and Thailand together account for 86% of revenues (Jouffray et al., 2019).

Insurance companies too, can act as powerful gatekeepers for sustainability. Sumaila et al. (2020) outline three key roles in particular: institutional investors – by choosing to support clients and projects that contribute to sustainability and divesting from those that do not; risks managers – by communicating recommendations for more sustainable practices to their clients; and risks carriers – by prohibiting or restricting access to insurance to clients that engage in unsustainable or illegal practice. An example here would be the coalition of insurers against illegal, unreported and unregulated fishing (Olano, 2017).

* See https://www.poseidonprinciples.org/finance/

** Joint Statement by the Multilateral Development Banks: Nature, People and Planet, online https://ukcop26.org/mdb-joint-statement/

Reconceptualizing risks

Each of these pathways of influence for the financial sector can complement each other, and in principle offer a forceful support for ambitions to accelerate climate and sustainability action. Addressing the connected nature of risks will not only require investors to engage in new ways and on new topics, but also new methods to assess such risks.

Translating climate risks including physical, transition and liability risks into actionable information for the finance sector remains highly challenging (NFGS, 2018; Fiedler et al., 2021). Additionally, improved accesses to data, risk disclosure policies, refined risk models and stress testing will have its limitations however. Chenet and colleagues (2021) argue that climate-related financial risks are characterized by radical uncertainty whereby the probabilities of different outcomes are impossible to calculate (see also Bolton et al., 2020). Such uncertainties can be created by for example multiple possible climate futures, and the complex pathways and propagation mechanisms that connect climate change to on-the-ground impacts. The fact that many of these risks lack historic precedent pose additional challenges to conventional financial risk management tools and indicators (Chenet et al., 2021; Crona et al., 2021; Kedward et al., 2020) because past behavior may not be sustained. This point has been made repeatedly by ecological economists exploring the connections between economic policies and the non-linear features of ecosystems and the climate (Crépin & Folke, 2015).

With these considerations in mind, a precautionary approach to financial policy and regulation could be more apt for our new planetary reality. Such policies focus on the stability of the system as a whole by mitigating the systemic financial risks, rather than on the regulation of individual institutions is one such proposed approach (Chenet et al., 2021; Kedward et al., 2020). One central feature of such policies is their empowerment of central banks and supervisory authorities by granting them with the mandate and tools to prepare for worst-case scenarios, and act in ways to reduce the likely emergence of instability before market participants recognize the surfacing of risk and adjust their behaviors. The identification, exclusion, or discouragement of activities that increase deforestation risks as one example, could be done via such policy tools (Kedward et al., 2020). A precautionary approach to financial policy and regulation requires the development of core indicators rather than on sophisticated risk modeling (Chenet et al., 2021). Chapter 4 elaborates on such indicators in more detail, and Chapter 5 explores the tentative influence of central banks and financial regulators on these matters. We put these recommendations in a broader context in the report’s final Chapter 7.

Chapter 3 – The Co-Evolving Nature of Inequality

Inequality is persistent, and associated with multiple social and health problems. Risks are being exacerbated by current Anthropocene challenges. As the world strives to accelerate action toward sustainability, inequality may, therefore, prevent socially sustainable solutions. High-income countries carry a larger responsibility for the new planetary reality and its detrimental consequences. This chapter focuses on the interplay between inequality and the biosphere, and high-income countries’ responsibility for ecological break-down. It presents the vicious cycles of inequality related to human and biosphere relations. The chapter also discusses the reinforcing role that tax havens have on inequality and environmental destruction.

Inequality is a persistent feature of today’s world, and brings about disparities in people’s ability to cope with a new planetary reality (Chapter 1). Moreover, high levels of inequality are associated with higher levels of societal and health problems, including physical and mental health, drug abuse, education, obesity, trust, and violence (Wilkinson & Pickett, 2009; Pickett & Wilkinson, 2015). This holds for both low- and high-income countries. The levels of income inequality differ dramatically between countries. In China, Europe, and the United States combined, the top 1% share 33% of total wealth today, while the bottom 75% share only around 10% (Zucman, 2019). Greater inequality in a society may lead to weaker economic performance and cause economic instability (Stiglitz, 2012). Furthermore, increasing income inequality may also lead to more societal tensions and increase the risks of conflict (Durante et al., 2017). Wealth discrepancies across countries can undermine the achievement of agreements and actions to tackle global problems such as climate change (Vasconcelos et al., 2014). High inequality is also linked to a lack of social trust (Kanitsar, 2022). As inequalities are persistent, they need to be actively counteracted to improve societal outcomes.

Inequity and vertical and horizontal inequality

While inequality simply refers to an unequal distribution of, e.g., resources, inequity implies that there are perceptions of a lack of fairness underlying differences in opportunities to acquire those resources. Inequity, therefore, highlights the need to account and compensate for unfair competitive disadvantages among individuals or systems to avoid reinforcing cycles of inequality. Inequality can be either vertical or horizontal. Vertical inequalities occur between people in a given society and can relate to incomes or educational attainment. Horizontal inequalities are inequalities between groups that share similar characteristics, for example, ethnicity or gender, and can be referred to as group inequality (Stiglitz et al., 2019). High levels of group inequality have been associated with discrimination, conflict, and lack of concern for the commons, which hampers socio-economic development and the handling of natural resources in ways that benefit society (Collier, 2007; Hillesund et al., 2018).

Inequalities and ecological breakdown

Differences in the wealth of nations are mirrored in the socio-economic and environmental trends of the ‘Great Acceleration’ (see Chapter 1; including, e.g., GDP, investments, and water use, all of which are higher in rich countries). Consumption in high-income nations whose populations represent 16% of the world population is responsible for 74% of the global excess use of materials, including biomass, metals, non-metallic minerals, and fossil fuels (Hickel et al., 2022). The USA alone is responsible for 27% of this global excess use, EU-28 high-income countries 25%, while China is responsible for 15%. The rest of the Global South (including low-income and middle-income countries of Latin America and the Caribbean, Africa, the Middle East, and Asia) is responsible for only 8% of the global cumulative material overshoot (Hickel et al., 2022, see Figure 5). Similarly, estimates of ecological footprint have also pointed to this disparity between nations where close to 50% of humanity’s impact on the biosphere can be attributed to some 16% of the global population (Barrett et al., 2020).

Figure 5 | Responsibility for excess resource use, 1970-2017. USA, Europe, and other high-income countries are responsible for 76% of excess resource use at the end of the analysis period. China is responsible for 15%, and the rest of the Global South is responsible for 8%. Source: Hickel et al., 2022.

{kind=link}

The interplay between inequalities and the biosphere

While the actions of a limited number of high-income countries and individuals have disproportionate impacts on the biosphere, the consequences of a degraded biosphere tend to have more severe impacts on low-income countries and/or individuals, resulting in amplified inequalities in society (Hamann et al., 2018). For example, Jafino et al. (2020) suggest that up to 132 million people will be pushed into extreme poverty by climate change by 2030. This increase is expected to result directly from the consequences of global warming, and from the costs of mitigation and adaptation. The expected impact on the poorest has been characterized as a “vicious cycle”, whereby initial inequality makes dis-advantaged groups suffer disproportionately from the adverse effects of climate change, resulting in great-er subsequent inequality (Islam & Winkel, 2017, p.2). This outcome stems from the varied exposure and susceptibility to climate change, as well as different abilities to cope with harmful conditions.

A more concrete example includes the Netherlands and Bangladesh, two low-lying countries, at high risk of rising sea levels due to global warming. The Netherlands, however, is a high-income country with capacities to build infrastructure and social preparedness to limit the impacts of rising sea levels. Bangladesh, on the other hand, does not have the capacity to develop large-scale coastal protection projects, and is therefore likely to suffer greater consequences from rising sea levels. Simultaneously, the Netherlands plays a much larger role in global warming, with current emissions of 8.8t CO2-eq. per capita compared to only 0.5t CO2-eq. per capita in Bangladesh (Climate Watch, 2020). Additionally, the Netherlands is also responsible for a greater share of historical emissions (Friedlingstein et al., 2021).

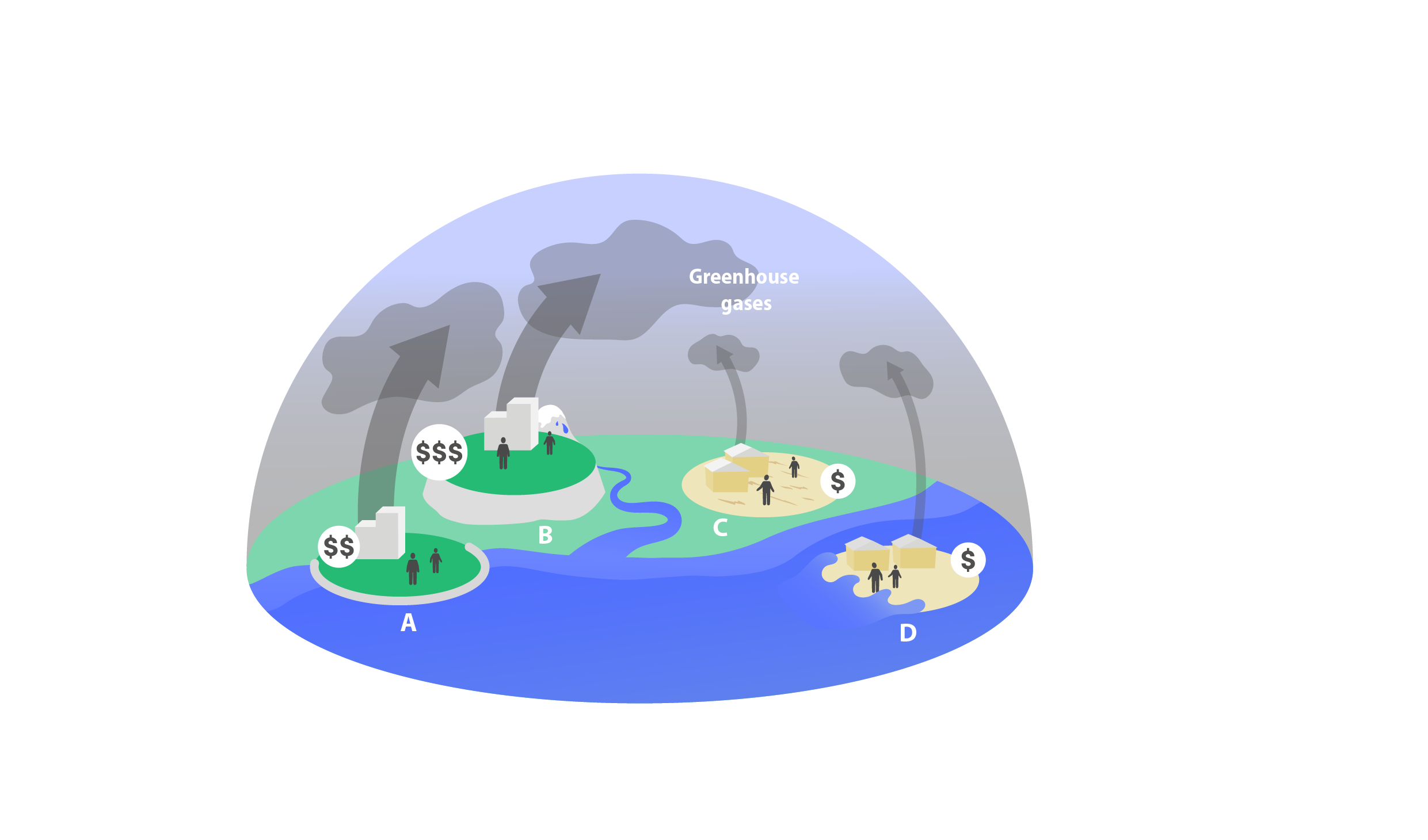

Hence, high-income economies, like the Netherlands, with disproportionate impacts on climate and the larger biosphere, are better prepared for dealing with risks, shocks, and surprises compared to countries like Bangladesh, which have had a relatively small historical environmental imprint. Gradual environmental change, more frequent extreme weather events, and pandemics, alongside limited capacities to mitigate consequences, risk worsening the consequences and exacerbating inequalities among countries. As referenced above, disproportionate pressures on the poorest may force people back into poverty and trigger social tension, conflict, and migration (World Bank, 2022). Given the likelihood of a rapidly changing planet with new systemic risks (see Chapter 1), the global community will need to address vicious inequality cycles (Figure 6) to achieve just futures on a thriving planet. The case study in Box 3 illustrates how historical heritage can give rise to unequal preconditions that limit resilience to shocks on the island of Hispaniola, home to both Haiti and the Dominican Republic.

Figure 6 | The skewed distribution of responsibilities and vulnerabilities. While many high-income countries (A and B) carry a historical responsibility for high emissions that are causing global warming and sea level rises, some of them (A) also need to significantly adapt to these consequences and have the ability to do so. Other high-income countries (B) are less vulnerable to the direct consequences of global warming and therefore might want to spend less to mitigate its consequences. At the same time, lower-income countries (C and D) have limited historical responsibility for ecological breakdown, but are hurt at least as seriously by consequences. With fewer resources to adapt to or mitigate impacts of climate change, C and D are significantly burdened by potential shocks they did not create. Such shocks may include sea level rises causing flooding, as well as extreme weather events causing droughts. This exacerbates the inequality between countries and will have complicated consequences in our globalized society. This simplification, however, hides the fact that the rich populations in lower-income countries heavily contribute to excess resource use.

{kind=link}

Box 3. Historical heritage giving unequal preconditions, limiting resilience

Haiti and the Dominican Republic are both located on the island of Hispaniola, with largely the same ecological prerequisites, but with very different societal outcomes (Sheller & León 2016). Haiti is one of the poorest countries in the Western Hemisphere, while the Dominican Republic has a thriving tourism industry. Despite the Eastern part of Hispaniola, where the Dominican Republic is located, having slightly more favorable agricultural prerequisites, historical events and unequal treatment by colonizing powers have been more determining factors in the unequal prosperity of the two nations (Sheller & León 2016). The devastating effects of the 2010 earthquake and Hurricane Matthew in 2016 on Haiti have resulted in an even further escalating gap between both nations, as Haiti has had limited means to rebuild or mitigate the consequences of extreme weather events. This illustrates how reinforcing mechanisms can generate major inequalities between two nations with largely the same ecological conditions.

Unequal access to biosphere resources

Access to biosphere resources may also be limited by unequal access to technology and know-how. For example, transnational corporations often extract, process, distribute, and profit the most from raw materials in low-income nations. They also have control over marine genetic resources by accumulating patents on genes, with a single corporation responsible for 47% of all registered marine sequences (Blasiak et al., 2018). On a global level, only a handful of transnational corporations are shaping the global intertwined system of people and planet through their extraction and use of ecosystem services (Chapter 5, Folke et al., 2019; Österblom et al., 2015). In addition, transnational corporations often benefit from low-income countries’ weak institutions and lack of environmental protection regulation (Schneider et al., 2020).